Fabric Finishing Agent,Chlorine Sdic,Sodium Dichloroisocyanurate,Sodium Dichloroisocyanurate Disinfectant Henan Kepeiao New Materials Co.,Ltd. , https://www.kopeochemical.com

Global smart meter market size

(A) European AMI cloth builds a leading position

Under the "20-20-20" agreement, the European Union requested that in the third EU's Energy Packages (2009/72/EC Electricity Directive), in 2020 AD, 80% of energy users must meet the requirement of using smart meters, prompting More EU countries have implemented replacement of electricity meters. The European market is nearing the end of the AMI dressing program in Sweden and Italy, which has slowed down the growth of the European market in 2009. However, it is estimated that after 2011, smart metering plans in countries such as Spain, France and the United Kingdom will be officially activated and begin to expand. Dress-up will resume significant growth.

(B) The United States began active AMI deployment in 2009

Driven by the US Energy Policy Act and the American Recovery and Reinvestment Act, US state governments, in collaboration with local power companies, began to actively carry out relevant construction plans based on local electricity usage. According to a survey by the Federal Energy Regulatory Commission (FERC), by the end of 2008, approximately 6.7 million smart meters were installed in the United States, accounting for approximately 4.7% of the total number of meters. It is estimated that about 52 million smart meters will need to be replaced in 5-7 years. .

(III) Asia is a potential market for the future

Asian countries and regions have a clearer outline of the AMI deployment plan in mainland China and Japan. Since mainland China began to announce the active deployment of smart grid planning in 2009, the National Grid has centralized bidding and procurement of all types of equipment. Among them, the Advanced Metering Infrastructure (AMI) has the fastest time to tender, and it has already conducted three rounds of approximately 28 million smart meter tenders. Japan's AMI import was first activated by Kansai Electric Power since 2008, and by the end of June 2010, 430,000 households have been reloaded, and meter data transmission has been carried out through its own established communications network. Tokyo Electric Power, the largest power company in Japan, is more conservative. The first wave of the 90,000 test plan is expected to be officially activated in October 2010. Others, such as Hokkaido Electric Power, Tohoku Electric Power, Chubu Electric Power, and Kyushu Electric Power, have also gradually activated the AMI construction plan.

Three major challenges in the AMI market

(I) Whether or not the cost can be reasonably reduced is the key to expanding the construction

The current deployment plans mainly focus on advanced countries such as the European Union and the United States. The average cost of each meter (concentration and information system costs) ranges from about 150 to 300 US dollars. These countries have paid more attention to the system in the initial stage of the pilot program. Sex and reliability, so it will not put price considerations in the first place. However, if we want to successfully expand the AMI deployment plan in the world, it will be critical whether the cost of construction can be lowered. In the future, with the deployment plans of various countries gradually expanding, under the accumulation of economies of scale and experience, it is expected that the cost of AMI construction will gradually decrease. In particular, the rapid start of the construction plan in mainland China will exert greater thrust on the cost reduction of AMI construction. Among them, the smart meter with the lowest technical threshold is the most. At present, there are about 600 home appliance manufacturers in China and the electricity meter industry chain is complete, with price competitiveness, and the Chinese government actively supports the promotion of the AMI construction plan. It is therefore expected that the smart meter technology capability of the Chinese mainland meter manufacturers will also increase. Will have a great impact on the market price of smart meters.

(II) The hidden dangers of privacy and security may become a major obstacle to the development of the AMI market.

The AMI system has privacy and security issues. AMI's introduction of home-use electricity information for all consumers is linked together via the Internet, and it is feared that the privacy-related information such as the type, quantity, and usage status of each family's electrical equipment will flow into the network. In the information security part, because AMI must handle a large amount of data transmission and analysis of power consumption, how to manage the security protection before the integrity of the power grid system is constructed to prevent the hacking system from stealing information and manipulating it is the management personnel's A big challenge. For example, the Dutch government began legislation in 2007 to force the complete replacement of smart meters. It is expected to complete the installation of smart meters for approximately 7 million users nationwide in 2013. However, due to the parliament’s consideration of smart meters, security issues will escalate. In the future, we will instead install voluntary smart meters instead of mandatory installations. This case shows that whether privacy and information security can solve and gain consumer trust can be one of the keys to the market acceptance of AMI in the future.

(III) Development of new business models for the electricity industry

The AMI deployment has a large cost burden for a single power company and does not help the power companies that sell “electricity†as their main operating revenue to increase their profitability. Therefore, whether other value-added services can be developed through the AMI system in the future will be one of the key factors for whether the power company supports AMI deployment and the development of the AMI market. Services that can be derived through the AMI system, such as: the lease of power companies to provide users with the "last resort" of communications solutions, provide users with energy-saving advice strategies, security industry cooperation with power companies to provide users with safety and other services such as gas and electricity home services Such as, so that power companies have the opportunity to transform from "sales of products" to "sales service", and then have the ability to continue to support AMI to expand the pace of construction and system maintenance.

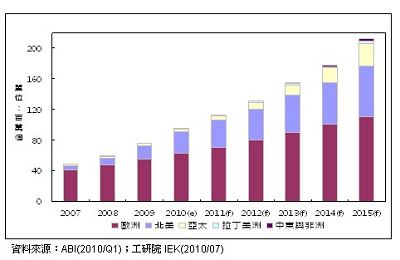

The promotion of smart grid deployment by countries is the key to the development of the Advanced Metering Infrastructure (AMI) industry. It will be the era of smart grids in 2010. According to the research agency ABI, the installed capacity of global smart meters will reach 9 in 2010. 5 million households, 13% more than the 76 million households in 2009, and the number of smart meter installations in the world will reach 212 million in 2015. It is expected that the major markets for smart meters will continue to be dominated by Europe and North America in the next five years. And Asian countries will become potential markets driven by mainland China (see below).